Payment gateway providers in the US offer technology that enables merchants to accept and securely process customer payments made via credit card, debit card, digital wallet, or other electronic methods. They act as intermediaries between customers, merchants, and banks, ensuring secure transactions.

Some top payment gateway providers in the US include:

1:Adyen: A global payments platform for enterprises that supports unified commerce across in-store, mobile, and online channels.. 2:Stripe: A developer-friendly platform with customizable payment infrastructure for online payments, subscriptions, and marketplaces. 3:PayPal: A traditional payment platform with eCommerce integrations and support for credit card payments and payment links. These providers offer various features, such as fraud detection, analytics, and multi-currency support.Regardless of the size of your business, a reliable payment gateway is crucial for providing a seamless and secure checkout experience – and for ensuring timely payments. The right provider goes beyond payment acceptance: It can help you reduce costs, expand globally, and simplify operations by consolidating payment, treasury, FX, and reporting into one unified platform.

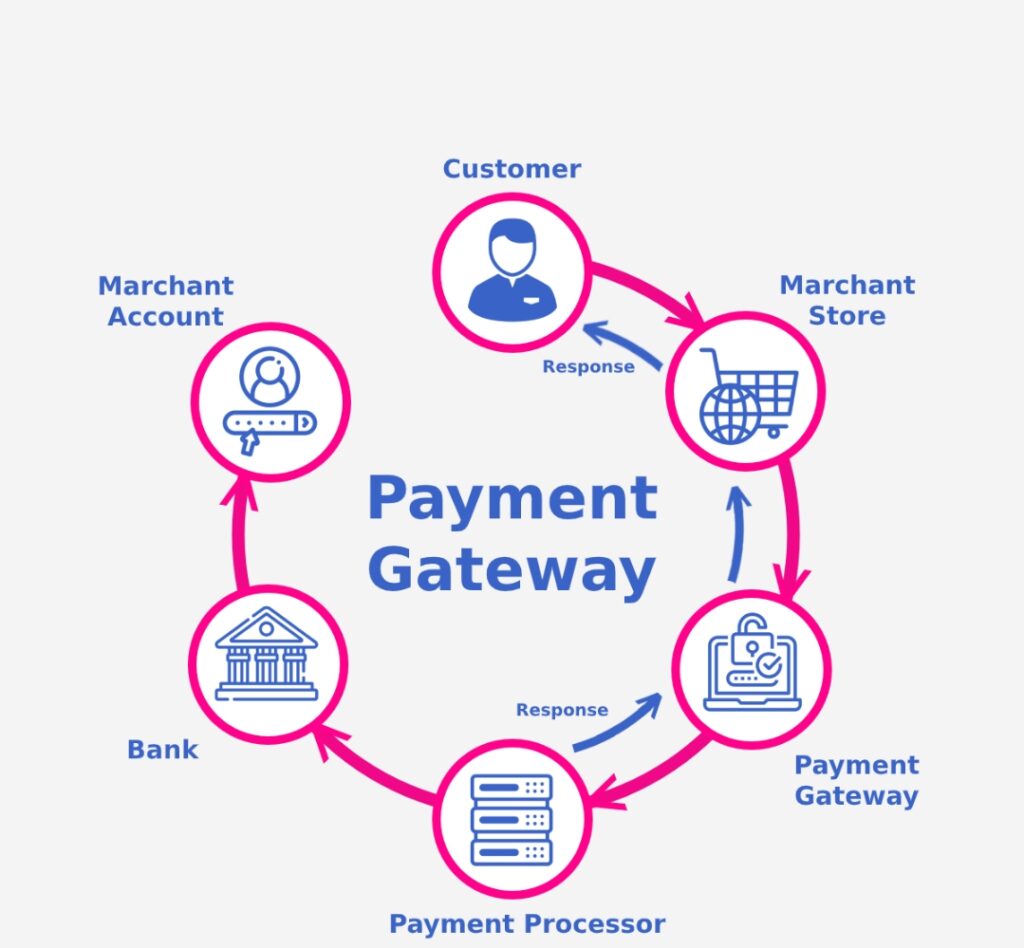

Here’s how payment gateways work behind the scenes after a customer makes a payment: Payment gateways act as intermediaries between customers, merchants, and banks. Here’s a simplified breakdown: 1. Customer initiates payment: Customer enters payment details (e.g., card number, expiration date) on a merchant’s website or app. 2. Encryption and transmission: Payment gateway encrypts the data and sends it to the payment processor (often the merchant’s bank or a third-party processor).. 3. Authorization request: Payment processor sends the transaction data to the customer’s card issuer (e.g., Visa, Mastercard) for authorization.. 4. Authorization response: The card issuer responds with approval or decline.. 5. Response to merchant: Payment gateway receives the response and forwards it to the merchant.. 6.Completion: If approved, the transaction is settled (captured) and funds are transferred to the merchant’s account.

Top features to look for in a payment gateway provider? It can feel overwhelming when you start comparing digital payment providers. To help, we’ve compiled a list of the most important features to look out for:

1:Processing location: Some gateways process transactions directly on your website, while others redirect customers to a separate payment page. For the smoothest checkout experience, look for a gateway with onsite transactions..

2:Cost: Pricing varies across different platforms. Pay close attention to setup fees, transaction fees, and any long-term contracts that may be associated with the service. .

3:Security: Look for PCI, DSS compliance, encryption, and tokenization to protect sensitive data.

4:Payment method support: Ensure support for various payment methods (credit cards, debit cards, digital wallets, etc.).

5:Global reach: Consider support for multiple currencies and international transactions if you have a global customer base.

6:Integration options: Check for easy integration with your e-commerce platform, website, or app.

7:Fees and pricing: Understand transaction fees, setup fees, and any other charges.

8:Reporting and analytics: Look for features that provide insights into transactions, sales, and customer behavior.

9:Customer support: Ensure reliable support is available when needed.

10:Recurring payments: If you offer subscriptions, look for support for recurring payments.

Compareing the top 6 payment gateway providers! Here are the top 6 payment gateway providers in Nigeria, compared based on their features, fees, and services:

1:NOWPayments: Supports 350+ cryptocurrencies, Visa, Mastercard, and PayPal, with fees as low as 0.5% for transactions without conversion.

2:Paystack: Offers multiple payment channels, including cards, bank transfers, USSD, and mobile money, with fees starting at 1.5% + ₦100 per local transaction.

3:Flutterwave: Supports 150+ currencies, with fees ranging from 1.2% to 3.8% for local and international transactions, respectively.

4:Interswitch: Provides integrated digital commerce and payment solutions, with fees typically around 1.5% for local transactions.

5:Remita: Offers payment services for businesses and government institutions, with fees around 2% for local payments.

6:VoguePay: Supports multi-currency payments, with fees starting at 1.5% for Naira cards.

When choosing a payment gateway, consider factors such as transaction fees, payment options, security features, and integration capabilities.

Questions to ask when onboarding a payment gateway provider? Here’s a set of questions you should ask before signing on the dotted line: 1: What currencies and countries do you support? Ask about multi-currency support, cross-border payment capabilities, and any currency conversion fees, especially if you operate or plan to expand internationally.

2: What security measures and certifications do you have in place? Ensure the provider meets industry standards, such as PCI,DSS, and ask about their fraud prevention tools and data protection protocols.

3:What additional features or services do you offer? Beyond basic payment acceptance, look for a provider that provides end-to-end financial tools, including foreign exchange, international transfers, same-day settlement, and spend management. These features can centralize your financial operations, reduce costs, and streamline the flow of money through your business. Fraud protection, analytics, and financial reporting tools are also essential value-adds to consider.

4:Can you support the payment methods my customers use? Determine if they accept your customers’ preferred payment methods, such as credit cards, Apple Pay, or Klarna.

5:What currencies and countries do you support? Ask about multi-currency support, cross-border payment capabilities, and any currency conversion fees, especially if you operate or plan to expand internationally.

Alternative payment methods: Your key to reaching more customers: Alternative payment methods refer to ways of paying that don’t use cash, checks, or a traditional international credit card scheme. Examples include AliPay, WeChat, PayPal, Apple Pay, and Klarna.There are many different types of APMs, including digital wallets, bank transfers and direct debits, BNPL services, cryptocurrencies, and prepaid cards.Offering a variety of alternative payment methods at checkout provides many benefits for businesses, including a smoother customer experience, better conversion rates, increased customer retention, higher levels of security, and easier expansion into new markets.Alternative payment methods, like digital wallets and buy-now, pay-later (BNPL) options, are becoming the norm. You’ll want to make sure that you’re offering them to provide the best possible checkout experience. As well as creating a frictionless payment environment, offering a variety of alternative payment methods can also expand your market reach and benefit your payment operations, giving you a competitive edge in a crowded market.

Different types of alternative payment methods? Customers usually expect to see several different types of alternative payment methods at checkout when they shop online. Here are some of the categories these may fall into:

1:Bank transfers:Bank transfers allow shoppers to pay for goods and services online by making a direct transfer from their bank account. Popular examples of bank transfer services include PayTo in Australia, iDEAL in the Netherlands, and PayNow in Singapore. These payment methods differ from manual bank transfers, which require customers to log into their bank account and manually input the recipient’s bank details.

2:Direct debits: direct debits are set up between customers and businesses to allow the business to pull funds from the customer’s bank account on a one-time or recurring basis. Direct debits are useful for recurring payments like subscriptions, memberships, and other bills.

3:Prepaid cards and vouchers:Prepaid cards and vouchers (such as gift cards from stores) are preloaded with funds and used like debit cards. Customers can complete payments without a bank account or credit card, and it can suit those who are new to digital payments, prefer not to share their personal and financial details online, or want to stick to a budget. Some examples include Paysafecard, a prepaid voucher, and Paysafecash, a cash-based voucher.

Why it’s good to accept alternative payment methods? Offering a variety of payment methods gives your customers options to pay in trusted and familiar ways. Here’s why else it’s a good idea to offer both mainstream and alternative payment methods:

1:Improves customer experience and increases conversion rates:Your business’s reputation doesn’t stop at the product. Customers want easy and reliable checkout options, with fast, secure, and familiar ways to pay.

2:Opens your business up to new customers:By accepting a variety of alternative payment methods, particularly local payment methods, you can attract new customers who may only want (or be able) to make purchases via a particular payment method.