Are you trying to figure out why the Cash App Borrow has stopped functioning? In this article, we have everything figured out for you. I guess you have attempted to use the Cash App Borrow button but were unsuccessful in doing so.

A few different issues can prevent the Cash App Borrow from functioning correctly. This section will explain all those factors and more information regarding the Cash App Borrow feature.

The Cash App originally began as a supplier of peer-to-peer money transfer services. Over the course of its existence, it has gradually gained additional capabilities as time passed. The exciting news for many people who use the Cash App is that it is now possible to borrow money from Cash.

On the other hand, it might be infuriating when you try to use the borrow button only to discover that it is not functioning correctly.

- Advertisement -

Why is the Cash App Borrow not working?

If you have access to the Cash App Borrow button but are unable to borrow money even though the button is present on your device, there is likely an issue with your account. If the Cash App Borrow is not functioning correctly, it is possible that the issues listed below are to blame.

There is a negative balance on your Cash App account.

The Cash App mobile application does not have the most recent version.

The Cash App views you as a potentially dangerous user.

You have violated the rules and conditions of the Cash App.

About cash app borrow

The Cash App is a popular smartphone application that comes packed with a variety of different functions. In addition to money transfers, bill payments, and investment options, the Cash app now also allows users to borrow money.

A new function called Cash App Borrow is now undergoing testing. Because of this, only a select few can use it. Through the Cash App Borrow button, you will be able to obtain a loan from the Cash App. You can take out a loan in the amount of $20 to $200.

The loan is compounded over the course of a year, and the annual percentage rate (APR) is sixty percent. This may sound excessive, but it is significantly lower than the typical interest rate for a payday loan. You will be required to repay the loan within two months and a fixed fee equal to five percent of the total amount.

- Advertisement -

If you are unable to repay the loan in full within four weeks, the Cash App will provide you with an additional grace period of one week.

After that, the Cash App will start adding 1.25 percent each week to your balance (non-compounding). Second, you won’t be able to get another loan if you’ve ever gone into default on one of your previous loans.

We are happy to list the best instant loan apps as those that will instantly lend you money (up to $50) without requiring excessive verification or form submissions. They come to your rescue in times of crisis, such as when you find yourself trapped and in urgent need of financial assistance.

When it comes down to it, these apps really can be a lifesaver in a lot of different situations. Some of these loan apps come with an interest rate, but they are not like the apps offered by loan sharks, which collect a significant amount of interest in a very short period of time. Please do not submit or collect money from such apps if you come across them since they may be operating unlawfully, and they may gather and sell your data to a third party. If you do come across such applications, please do not submit or collect money from them.

In the following paragraphs, we will introduce you to the top app for instant loans, which allows you to borrow at least $50 or less, such as $25, in a matter of minutes. These rapid loan applications provide you with a repayment period of thirty days, and the interest rate that they charge is not particularly expensive.

Best $50 Instant Loans Apps (2026)

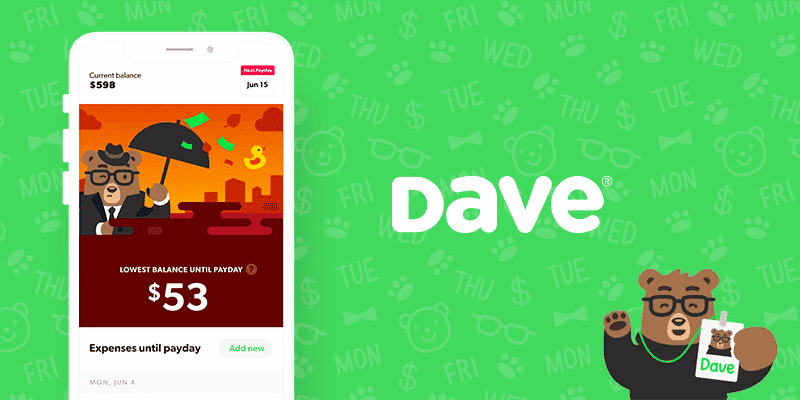

1. Dave

dave loan app

Dave is another instant loan app that lets registered users get up to $250 in cash right away. But the amount you get from Dave depends on your account history, average balance, and loan credit score, among other things.

You can also make a direct deposit into your Dave account so that you can pay it back in full when your loan is due. You can pay back the loan in parts or all at once, whichever you prefer. But you should set up a payment plan before the loan is due.

Dave costs $1 per month to join, and you can use ATMs and debit cards for free as long as they are in the network.

2. Earnin

Earnin loan app

Earnin is an app that can give you an instant loan of up to $100 per day or $500 per pay period. There is no fee for the loan, but the transfer rate is $2.99. The interest rate is $0, and it will take between one and three business days for your loan to arrive. You can use the more advanced features of Earnin if you link it to your bank account.

When you link Earnin to your bank account, it will automatically take back the money you borrowed when your direct deposit paycheck comes in. You can give Earnin a tip for the money it gave you, and you have to be working on using Earnin.

3. Chime

chime loan app

Chime is a fintech banking app that lets people open spending accounts that require a certain minimum balance. Not only that, but they also give their users instant loans from $20 to $200. This means you can get a loan right away for $25, $40, $50, $100, or even $200 without any trouble.

You do not need to undergo a credit check in order to make an instant deposit of $200 when you register an account with Chime. Despite this, they will still utilize a variety of procedures to evaluate your application before giving it the green light. Chime also offers its customers a free debit card that does not incur any fees when used to make purchases.

4. PaydaySay

paydaysay loan app

PaydaySay is another app that can give you an instant loan of up to $50. The app connects people who need money with people who have money to lend. This means that you can sign up for the app as either a borrower or a lender. You can borrow between $100 and $200. But the borrowed money needs to be paid back in full by the due date.

You must pay back the loan on time so that the lender gets their money back. But if you don’t pay back the loan, interest will be added to it. PayDaySay, unlike Chime, checks your credit before giving you money. Also, the interest is a bit high since it’s a person lending you the money.

5. Brigit

brigit loan app

Brigit is an app that lets you borrow money and connect it to your bank account. This app lets you borrow between $50 and $250. It connects to your bank account, so it can only approve your amount based on what you do with your bank. After you borrow money from Brigit, your advance repayment schedule is set up for you automatically.

The good news is that you can choose to pay back your loan early or extend the time you have to pay it back. This budgeting app costs $9.99 per month and does not check your credit or charge you interest.

6. MoneyLion

moneylion loan ap

MoneyLion is a banking app that can give you a $250 cash advance through a feature called “Instacash.” You can borrow anywhere from $25 to $250. To use MoneyLion, you must have an account that has been open for at least two months, show that you make regular deposits, and have a working account.

You can use your MoneyLion account or an outside checking account to pay back an Instacash loan. How much you can get will depend on how long you’ve had a MoneyLion account. The longer you have a bank account, the more likely it is that you will be able to get a higher advance loan.

Alternative To Instant Loan Apps

Why not try something else instead of looking for an app to get a $50 loan right away? If you do these things, you’ll always have $50 in your bank account if you follow these steps. You may be wondering what else you can do. So, here are the answers:

Have an Emergency Fund

You must have heard people tell other people to have an emergency fund or start one. So, it’s the best piece of advice ever. Having an emergency fund will help you a lot in a situation like this. We know that this may be hard for a lot of people. But if you can save $10 per week, you’ll have up to $40 in a month, which is close to the $50 instant loan you want.

- Advertisement -

This means that in two months, you could save up to $80. You can save this money for a rainy day. You can always use them in similar situations and then get new ones. What if you don’t have a job? What should you do while you don’t have a job?

Start A Side Hustle

Start a side business while you wait for your dream job. This will help you save money and have more than just $50 on hand in case of an emergency. We live in a modern world where all you need to work is a smartphone and an internet connection.

You can do a lot of different things on the side, like sell things online or look for work on sites like Fiver, Upwork, and many others. Here are some ideas for things you can do on the side.

Deliver food for Instacart or DoorDash

Driving for Uber, Bolt, or Lyft

Teach language online.

Teach Yoga

Write an eBook.

Find (legit, trustworthy) gigs on Craigslist.

Find gigs on Fiverr.

Babysit

Sign up for TaskRabbit

Sell items online

Be a DJ

Get a job as a server for a restaurant that will let you start immediately.

Deliver pizzas

Conclusion:

A $50 instant loan application is a fantastic way to free yourself from debt pressure. You should be aware that there is an interest rate associated with this. While some apps might not be worthwhile, they might also require a monthly subscription fee. Please borrow only what you can afford to repay before installing any apps, and make sure to read the terms and conditions.

Cash App Borrow – Cash App is a mobile app for sending money backed by Square, the same company that sells millions of dollars worth of “Minecraft” pickaxes. It’s also where I’ve been getting loans for tens of thousands of dollars lately. And so can you!

If you’re in an area where cash works, it’s just like Venmo or any other peer-to-peer payment transfer service, except it’s way better. Here are some explanations:

You’re probably saying, “But why would I want to borrow money if I already have a credit score of 650 or more?” Why would I want to make things worse with my money? As always, many reasons for this have nothing to do with me:

You want a fun side business that makes you a millionaire in secret. Everyone will be jealous of you if you walk around with a bag full of $100 bills, and they don’t know it’s because you’re an Uber driver or maybe a trucker. You are having trouble paying your bills, and peer pressure isn’t helping.

- Advertisement -

You like to get drunk, and it’s nice to be able to buy more alcohol without using your credit card or borrowing money from friends. You want to use what other people have against them for fun, and this is an exciting way to do it if you already own something that can be used as collateral.

Cash App

It can be hard to borrow money because:

People on your social network might always try to force you to give them money. If they do, you should ignore them and look for people who don’t need as much help. You should keep your cash app balance pretty high because you never know when someone will come up to you and ask for $20 for a cab. If other people want their money back immediately, you can’t repay the loans on your schedule.

Does Cash App Let You Borrow Money?

Yes, it’s clear from their FAQ that it’s legal in most states. There are a few situations where you can’t lend money to people, but if you live in the U.S., it should work for you.

It is still in the testing phase, so not everyone can use it, and loans can only be between $20 and $200. Loans are given out immediately and must be paid back in four weeks or less. But if you have a debt for a long time, it may cost you more. The Cash App charges a flat fee of 5 percent to borrow, plus an extra 1.25 percent every week after the grace period.

- Advertisement -

If you know that a Cash App Borrow loan is meant to be paid back quickly, the new tool could help you out when you’re short on cash.

What You Need Before Borrowing Money in Cash App

Your debit card or bank account, if possible. If you don’t have one, make one before going any further!

A Cash App card (optional).

A plan for what you’ll buy with the money you get from something else, like your rent or something.

How to Borrow Money in Cash App

Right now, not everyone can use the Cash App Borrow. Checking is the only way to find out. To borrow money from Cash App, follow these ten easy steps:

Launch the Cash App.

Tap the Cash App balance in the lower-left corner of the screen.

Go to the section called “Banking.”

Look for the term “borrow” in the dictionary.

If you see the word “Borrow,” you may apply for a Cash App loan.

Tap “Borrow.”

Choose “Unlock.”

You can find out how much you can borrow from Cash App.

Please read the user agreement.

Accept a loan from Cash App Borrow.

What Other Options Do You Have for Borrowing Money Online?

OppLoans

OppLoans is an online service that helps people in the U.K. get quick and easy cash loans. This is an excellent place to start if you want to borrow money because you need cash immediately. Since 2007, the company has been helping people and small businesses. It can give loans of between £50 and £15,000.

LendingClub

LendingClub has many personal loans, ranging from $1,000 to $40,000. This advanced app could be the best way to get a low-interest loan online if you have a steady source of income and can pay back the loan in monthly payments for up to five years.

- Advertisement -

Empower

Empower is an online platform for personal loans with lower interest rates than those of traditional banks. Empower may be the best place to get a secured or unsecured loan if you have good credit. The company has helped more than 35,000 customers improve their financial situation with personalized loans for debt consolidation and other reasons.

Cashnet

Cashnet gives people and small businesses instant cash loans. You can get a loan from $100 to $5,000 and choose how to pay it back in a way that works for you. There is no need to check your credit, and the approval process is easy and quick.

LendingPoint

Since 2009, LendingPoint has been offering private installment loans to consumers. The company only works with A-rated lenders. You can borrow money for any reason and pay it back over time by making payments every month. LendingPoint has fixed rates, terms, and fees that are easy to understand, making it quick and easy to get a loan online.

MoneyLion

MoneyLion gives out personal loans for things like consolidating debt, making home improvements, buying new things, and more. Even if your credit isn’t the best, you can get money in two business days.

- Advertisement -

Wonga

Wonga is one of the most popular online lenders in the U.K. Its easy-to-use platform has helped more than 4 million people get affordable loans. No matter why you need money, Wonga can help. Just make sure to look at the fees before you sign up.

If none of these options work for what you need money for, try searching Google. There are a lot of people who need money right away because they are in a bind. If you can figure out who you can trust and can’t, you can make the best choice for yourself.

There are many ways to borrow money, and each has its pros and cons. Know what you’re getting into before you borrow money. Researching your options can make it easier for you to get a loan.

How Much Does it Cost to Borrow Money in Cash App?

With Cash App Borrow, there are no fees for applying or getting the loan but a flat fee of 5% of the amount borrowed.

In 24 hours, Cash App Borrow will take the loan amount out of your account. When you pay back Cash App Borrow, the fee will be taken out.

- Advertisement -

How Do I Repay my Cash App Borrow?

When it’s time to pay back the money you borrowed through the app, choose “re-borrow” or “cash advance” to see how much you’ll have to pay back next. You can pay it back in full at any time, or you can pay it back in monthly installments.

If you pay back less than the total amount borrowed, there is no penalty, but you’ll have to pay more if you borrow more. The fee is 5 percent of the total loan amount, plus an interest rate that depends on your state and how much time has passed since the loan was given.

With the on-the-go reminders feature of the Cash App Borrow, it’s easy to keep track of payments. The app will remind you when a payment is due if you forget.

What Happens If You Don’t Repay Your Loan?

You will run into trouble. Cash App will cancel all your Cash Card purchases immediately, and you won’t be able to use your account to buy anything until you pay back your loan with interest.

- Advertisement -

Are there any pro tips for using Cash App Borrow to its fullest?

Yes! To make the most of your Cash App account, follow these five easy steps:

Pay back any loans you take out.

Fraudsters may try to hide the fact that they are fraudsters, so don’t do anything with them.

If you already have too many loans, don’t take out more. It’s hard to get out of that hole, and sometimes it’s even impossible.

Don’t use the service in the wrong way!

If you have an emergency, call customer service immediately.

Final Thoughts

Cash Apps Borrow is an easy way to get money when needed. It’s very safe, and it can save your life in a lot of situations! Please ensure you always pay back the money you borrow, don’t fall into the debt trap, and use all the tips we’ve given you here.

There is a FirstEdu loan accessible to private school owners who need additional finances to ensure the proper operation of their educational establishments.

Loan Features

Available to all CAC-registered private schools (either Government approved or not).

The duration of a tenor ranges from 90 days to a year (terms and conditions apply).

N20m is the maximum loan amount.

Schools that are registered with CAC but do not have Ministry of Education clearance can borrow up to N2 million for 90 days each.

Funding for the use of school cars (new and fairly used)

Up to N20 million in 24 months of asset acquisitions.

FirstBank has agreed to act as collateral for the payment of the student’s tuition.

A bank account must have been maintained by the school for at least a year.

A school must have at least 100 students.

Benefits

An easy way to get the money you need for your business’s operating capital.

Documents Required

Proof that the school has been approved by the government.

Where appropriate, the school’s Memorandum and Articles of Association (MEMART).

There are records to illustrate how long the school has been in operation.

Records indicating the total number of students enrolled at the institution.

The bank may demand further paperwork.

Who Can Apply

Without Ministry of Education clearance, schools that have CAC registration can borrow up to N2 million for 90 days.

A’ level Tuition Providers who are registered with both the State Ministry of Education and the Corporate Affairs Commission are permitted to operate.

How to Apply

For those interested in applying for a FirstEd Loan,

LSETF

Brief Description

Only schools and relevant educational institutions (ME and SME categories only) with a minimum student population of 100 are eligible for this 5B intervention fund (one hundred).

Interest Rate

The fixed interest rate is at 9% per annum (all-inclusive).

Loan Tenure

Twelve (12) months for loans of less than or equal to N1,000,000.00.

N1 million and above loans have a grace period of 24 months.

Loan Amount

Maximum of N5 million.

Eligibility Requirements

Must be a Lagos State resident to apply

Registration with the CAC is required, as is at least one year of operation at the school or training institute in question.

Have a minimum of 100 pupils enrolled for the entire year.

Must have two (2) well-off guarantors who can back up the loan.

a good credit history

Documentation of Tax Obligation and Payment

Required Documents

Application form

CAC Documents

6 months bank statement

LASRRA ID (Lagos State Residency Registration) of the borrower

Evidence of Tax payment

Bank Verification Number (BVN)

One (1) Guarantor who must have verifiable LASRRA registration – (Below N500,000)

Two (2) Guarantors who must have verifiable LASRRA registration – (Above N500,000)

Are you planning to leave the United Arab Emirates while you are in debt? The process may be difficult, but you may have legitimate reasons. Today, the United Arab Emirates has enacted rigorous financial laws to ensure that all borrowers pay their loans, a change from the past when many people departed the country with unpaid debts.In order to help you prepare for your departure from the United Arab Emirates, we have compiled a comprehensive list of things you should know. Foreign investors in the United Arab Emirates owe money to the UAE in three different ways, according to our findings. Your departure from the United Arab Emirates will be impacted by these debts.

1. Leaving UAE with Personal or Car Loan

When a bank gives you a loan in the UAE, they ask for a security check for the amount of the loan. The bank also keeps copies of signed agreement reports that explain the terms and conditions in more detail. If the due date passes, the debt will be collected in a strict way without telling you. But if you leave the country, your banks will send all of the security checks back to the bank in UAE.

What happens if you don’t have any money in the bank? In UAE, it is a crime to have security checks that can’t be cashed because you don’t have enough money in your account. So, the bank might file a criminal complaint against you, which would make you a fugitive. The agreement you signed with the bank also gives them the right to sue you in court. If you are outside of UAE, the court may order that you be locked up as soon as you get back.

You can still leave UAE with a personal loan, but you have to follow their rules for making payments when you’re not there. First, you have to call the company you owe money to and explain what’s going on. You can ask for a new payment plan that fits your location and how much you can pay each month.

If you have a good history of paying back loans, the bank may let you leave the country with their money. But the bank might need some extra paperwork to process your request. Before they let you leave the country, they always write everything down so you can’t just ignore them.

- Advertisement -

2. Leaving UAE with Mortgage

If you own a home in the United Arab Emirates, you might have to pay off your mortgage before leaving the country. Some banks want you to pay in full, but others let you leave and set up a payment plan from somewhere else.

If the bank wants you to pay the full amount, you have three choices, which are;

Paying the whole mortgage balance using your means

Selling the property to repay the mortgage

Re-financing with a non-resident mortgage through a different bank.

If you have a mortgage and want to leave UAE, the terms and conditions you and the bank agreed on will apply. But you can change your mortgage from one for a home to one for a business. To pay your mortgage while you are away, you will have to sign an agreement with the bank and keep your UAE bank account open.

But this bank account for non-residents will be with the same bank as your mortgage. You will need to make sure that this account has enough money in it to pay for your mortgage. On the other hand, the bank might put you on a list of people who haven’t paid their bills. If you rent out the property, make sure the rent goes into the account so that the debt can be paid off.

If you don’t pay back your mortgage in UAE, you could lose your home, just like if you didn’t pay back any other loan. How you pay your mortgage doesn’t matter to the bank. So, you can use any of the above methods as long as they don’t break the rules of the financial institution.

- Advertisement -

3. Leaving UAE with Credit Card

If you don’t pay your credit card bills, you’ll have to pay more in interest and other fees. What happens if you leave UAE without paying off your credit cards? If you don’t pay your credit card bills once or twice, you may have to pay high interest rates or late payment fees. On the other hand, if you don’t pay your bills for a few months, the bank can sue you.

The Central Bank of UAE says that if you don’t pay your credit card bill for six months in a row, the bank will put you on a list of people who haven’t paid their bills. Without your permission, the bank can use any legal method to get its money back.

If you don’t do what the bank wants, it can send debt collectors to get in touch with you. Debt collectors will track you down as far as your house and remind you to pay off your credit card debts. Also, if the bank takes the blank checks but there are no funds in them, the bank can press charges against you.

According to the laws of the UAE, people can be fined and put in jail if;

Give cheques with no or less drawable balance.

Withdraws all or some of the balance, making it insufficient for settling the credit card debt.

Give the wrong signatures to prevent withdrawal of cash.

If the bank brings charges against you, you also can’t leave the country. You won’t be able to enter or leave the country. If you have already left the country, you will be held when you come back into the UAE. What can you do if you have credit card debts and want to go back to UAE?

- Advertisement -

You have to ask the country’s authorities if there are any charges against you or if you are not allowed to travel. After you know your status, you can take your time to talk to the bank about other ways to solve the problem without using sanctions. Before you go back to the UAE, give yourself time to pay off the debt completely. So, you’ll be free of debts and able to legally work in and out of the country.

Consequences of Trying to Leave UAE with unsettled Debts:

As we’ve already talked about, leaving the UAE with debt is a risky thing to do. If you have debts and want to leave the country, it is usually a good idea to talk to your lenders. Below, we talk about what will happen if you leave the UAE while you owe money.

UAE Immigration Officers Blocks your Movement

Not unless you move quickly enough before the bank tells the court about you and puts a travel ban on you. If you want to travel safely, make sure your loan payments are current and that the government hasn’t put you on a wanted list for loan default. Also, immigration officers are told right away so they can stop you from leaving the country without paying off your debts.

Your UAE Bank Remains Activated

If you owe money to the UAE government, you can’t close your bank account. The bank account becomes a non-resident account, which lets you keep paying your loan while you’re out of the country. You can only close your bank account if you have paid off all of your debts and still don’t want to use it.

- Advertisement -

You May Have a Case to Answer

Getting taken to court and being charged with a crime is the worst thing that can happen. If you are a foreign investor in the country, it wastes your time and hurts your reputation and business brand. If the bank presses charges against you for not paying back your loan, you could go to jail or have to pay a big fine. So, it’s smarter to pay off your debts or use your power to convince the bank to give you more time.

Direct Deductions and Auctioning

No matter where you live, the bank may find other ways to get their money. They can take their loan right out of your pay without telling you. When you don’t follow their rules, they take this step.

The bank may also send auctioneers to your home to get their money back. You can sell anything valuable to pay off your bank debt. I’m sure you wouldn’t like it if you couldn’t control your own property. So, the best thing to do is pay off your debts instead of trying to avoid them.

Measures to Take to Re-enter UAE After Defaulting:

Many people want to go back to the UAE after leaving for business elsewhere. There is still a chance that you’ll be able to go back and keep running your business. Here are the steps you need to take to get into the United Arab Emirates again.

- Advertisement -

If you decide to leave the UAE for another country, it’s best to find someone you can trust to keep running your business there. Find someone you can trust to handle your money. You will need to give the bank a power of attorney or a well-written letter. So, even though you have debt, you will be able to leave the country because the bank will hold someone else responsible for your money.

You can easily go back to your country because no case has been filed against you. Then, you can take care of your businesses.

Get Clearance Certificate

When you have paid off all your debts and want to go back, the bank should send you a clearance certificate to show that you are no longer “wanted” for defaulting. Also, the bank needs to clear your name with the national police and immigration to let them know that you are now free.

Also, make sure you get a letter from the police saying that they dropped the charges against you. If you need to involve the embassy, you should be patient and follow their rules before you go back to your country.

Once the bank clears you, make sure to get it in writing so you have something to show as proof. If you have a lawyer, they will handle the paperwork and it will be legal for your name to be cleared.

- Advertisement -

If the person you made the deal with leaves the bank, you have to follow the written agreement. You will have proof that the bank stamped and signed it on a certain date. So, no one will have to start paying back because they didn’t have enough proof that they were cleared.

Negotiate the Repayment Method

If you’re not in the UAE and you owe money there, you decide to talk to the financial organization about the payment terms so they’ll let you go back. You need to hire a good lawyer to represent you in the negotiation if you want to win. Also, having a legal team there makes sure that everything agreed upon at the table is put into action, which is good for both sides.

If the bank agrees to your terms of payment, you won’t be able to leave the country and you won’t have to pay the fees. Even though it costs money to hire a lawyer, it’s worth it because you’ll be free.

After you clear things up with the bank and the police, you can go back to the UAE. No creditors will come after you, and you won’t have a record of not paying back loans. It’s nice to know that the bank can still give you a loan after you’ve paid off the first one.

- Advertisement -

Bottom Line:

You might want to leave UAE for any number of reasons, including changes in the economy, illness, homesickness, or anything else. As we’ve already talked about, it’s against the law to leave the country with debts, especially if you haven’t told the bank.

Unfortunately, leaving won’t help because the government will still find other ways to get their money back. All the banks in the world will know that you owe UAE money, which means they can come after you without your permission. So, the safest thing to do is work out a fair deal with the bank to pay off your debts and be free to go back to the country.

The NPF microfinance bank may have difficulty transferring your approved 2022 National Youth Investment Fund (NYIF) into your bank account if you are one of the many. We’ll show you how to transfer your NPF Microfinance Bank’s NYIF loan to your bank account in this article.

As a method to support the country’s youths, the Nigerian federal government launched this loan opportunity, which has already been approved.

Meanwhile, we have provided you with all the necessary processes and procedures to ensure that the loan from the NPF is transferred to your bank account successfully. In the meantime, let’s take a look at what led up to its creation.

Things you should know about the Nigerian Youth Investment Fund (NYIF)

Nigeria’s federal government launched the Nigerian Youth Investment Fund in partnership with Nigeria’s Federal Ministry of Youth and Sports (FMYSD) and began accepting applications for the program in 2020. The fund has helped many Nigerian youths and continues to do so today. Over the course of the loan’s existence, the same department has approved over 25,000 recipients.

NPF microfinance bank, Lapo, and Baobabs remain the permitted banks for NYIF payment, making it easier to reach the beneficiaries after overcoming the issue that the initial group of beneficiaries experienced from NIRSAL.

- Advertisement -

Because it has the support of the Nigerian federal government, all lucky beneficiaries must receive their funds only when they have completed the necessary tasks.

Lapo and Baobab NYIF Disbursements vs. NPF Microfinance Bank?

For the purpose of the NYIF, both banks distributed the identical amount of NYIF loan assigned to beneficiaries, despite the fact that their names are very different. As previously said, they all serve as a conduit for the distribution of NYIF to beneficiaries, and this will remain the case unless the originator of the plan changes his or her mind, in which case I will notify you. It is up to you to keep an eye on our post and make any necessary corrections.

Transferring NYIF Loan from NPF to your account

This is the most important portion of the article, and it’s why I’m writing it. I’m going to go over the process of moving monies from NPF Microfinance Bank to your NYIF account in order to clear up any lingering questions. The steps are as follows:

1. Online banking/internet banking

Using the NPF website and first clicking https://ibank.npfmicrofinancebank.com/ after successfully logging in, the only difference between this and the typical online transactions we perform every day is the NPF registration.

- Advertisement -

A) Creating an account on the website is as simple as entering your NPF account number and password. That’s what happens when you click “Create a new account” on the page.

B) As soon as you’ve entered your NIN number, date of birth, and photo, you’ll be prompted to sign your name, as well.

C. Once you’ve completed the steps required by the site, you’ll have to wait a full day (24 hours) before your transfer is approved.

2. Making Use of the USS Code

When it comes to making a transfer, most recipients find the process of dialing *5353# to complete their transaction to be simple. The network’s fluctuation or unavailability is a significant disadvantage of the code technique that users encounter when conducting transactions. In addition, the employment of code is the most efficient method for reducing both time and energy.

3. Download/Install the app

The NPF microfinance bank has its own app, much like any other bank, and it follows the same steps as internet banking, including filling in the blanks and creating an account. Many individuals have tried to download the software from the Google Play store, but it has been withdrawn. Visit HERE to download the NPF Microfinance Bank official app.

Since the NPF app and website both include an option to sign up for an account, if you don’t do so, you won’t be able to transfer your money.

- Advertisement -

Do you think NYIF registration will be available in the future?

In light of Nigeria’s government’s goal to eliminate youth unemployment and encourage entrepreneurship, the site will soon be open for future beneficiaries, and the government will not hesitate to explain why it didn’t work out in the place where it didn’t work out.

Are you are business owner? Is your business or household affected by lockdowns brought about by the lethal Covid19 pandemic? If your answer is ‘yes’, you can fill out a Covid-19 Loan Support Form to get funds from the federal government, through the Central Bank of Nigeria (CBN).

Requirements to get Covid-19 Loan Support in Nigeria

Once the form page opens, select the reason for the loan application, then submit.

There are different types of Covid19 loans

Households: their livelihood are negatively impacted.

Microenterprises: Existing Enterprises affected by the pandemic.

SMEs: Enterprises that want to take advantage of opportunities arising from Covid19.

After completing the loan application, it will display “Thank you! Your application has been summited successfully“.

Then after some days, you will get the notification that your application for the loan has been approved. If you have a question, kindly go to the comment section below.

UBA Personal loans assist UBA Salary Account holders with Savings and Current to pay for unexpected needs, such as medical bills, and make home upgrades. Upon receipt of the relevant papers, the UBA Personal Loan facility requires approximately 48 hours for loan disbursement following a request for a personal loan.

Borrowers can take advantage of a flexible loan duration of up to 60 months. The loan amount ranges from N100,000 to N30 million, based on your earnings and other stipulations. The interest rate is as low as 20%, and there is a one-time management fee of 1%, granting you access to up to 50% of your debt service ratio (DSR).

How do I know if I am eligible for a loan?

To qualify for a UBA Personal loan, the following requirements must be met:

You must be a verified member of your organization’s personnel.

You are required to have a UBA Salary Account.

Your employer must be on the list of approved Personal Loan organizations.

What documents am I required to provide to obtain a UBA Personal Loan

To qualify for the UBA Personal Loan, you must present the following documentation:

A duly completed Loan Application Form.

A copy of your pay slip and bank statement of account indicating salary inflows in the last 6 months.

A letter of awareness from your current employer.

UBA Personal Loans Requirements

Before you can apply for a personal loan from UBA, you must present the following papers.

Functional savings or current salary account

Duly completed loan application form.

Valid means of Identification (international passport, national driver’s license, national id card, and voters card).

Employer’s undertaking to domicile salary with UBA.

Duly accepted offer letter or employee inquiry form (The offer letter should contain

Employee Name, Employee Job Description/Position; Nature of Employment (Permanent or Contract); Employee Job Status (Confirmed or unconfirmed).

Copy of the obligor’s staff ID.

How to apply for UBA Personal Loans

You can quickly apply for a personal loan from UBA Bank by using the dedicated lending site “Integrated Credit Express (ICE)” or by visiting one of our Business Offices. Additionally, you may contact your Relationship Manager for assistance.

Submit a completed loan application form with supporting documents at any branch

Execute an offer letter detailing the loan terms and requirements, following loan approval

Loan will be disbursed into a salary account domiciled with the Bank.

Upon receipt of the relevant papers, the UBA Personal Loan facility requires approximately 48 hours for loan disbursement following a request for a personal loan.

Are you looking for Payday loans that are available in all Canadian provinces and territories?

We select the best payday loans based on their reputation and quick and dependable service that can get you the money you need in just a few minutes.

Payday Loans can be used to replace a household appliance, pay a medical cost, or put down an apartment deposit (both salary and non-salary earners). As long as you can prove your ability to pay back the loan, you can use Payday Loan to get a short-term, high-interest line of credit.

Instant digital loans for salaried individuals who match the bank’s Risk Acceptance Criteria (RAC) are classified as unsecured personal loans because no collateral is required.

As long as the province of the borrower has implemented proper provincial legislation on the providing of payday loans, cash advance loans or payday loans in Canada are legal.

- Advertisement -

What is Payday loan

Taking out a payday loan is a short-term solution in the event of an unexpected payment, auto repair, or house maintenance. Payday loans and cash advances are other names for it. Take out a loan for the amount you require right away, if approved. On your next paycheck, you’ll be required to repay the borrowed funds plus a service fee.

List of Payday lenders in Canada

In Canada, there are a slew of payday lenders, but we’ll focus on a select few that can assist you fulfill your immediate financial demands.

1. Focus cash loans

As opposed to other loan companies, Focus Cash Loans doesn’t perform any sort of credit checks. They treat each loan application as though it were a one-on-one situation. With Interac e-Transfers, you can have your money in a matter of minutes after you’ve been accepted. Borrowers must apply online from the comfort of their own home or office at any time of the day or night, including weekends, Saturdays, and Sundays.

2. Icash payday loan

In order to apply for an iCASH Payday Loan, you don’t need any paperwork, and the entire process can be completed online. It is possible to have an e-transfer from the internet direct lender to your bank account in just a few minutes.

- Advertisement -

3. GoDay Payday Loan

A fast online payday loan between $100 and $1,500 is available from GoDay Payday Loan, while a long-term installment loan between $1,000 and $15,000 is available. As soon as you’ve been approved, you’ll be able to use your payday loan. Loan terms range from one to sixty-two days long.

The automated system of the lender accepts and processes applications for online payday loans, short-term loans, cash advances, and installment loans around the clock. Both consumers with terrible credit and those with no credit are eligible for the loan.

4. Cash Money Payday Loan

Cash Money Payday Loans have hefty interest rates and fees. Loan amounts are based on a borrower’s net income and other restrictions. In Alberta, Manitoba, and New Brunswick, promotional pricing are not available. From 5 to 40 days, you have the option of taking out a loan of $100 – $1,500 for a total loan amount.

Unemployment, disability, Canadian child benefit, and social assistance are all accepted by the internet direct lender.

5. Money Mart Payday Loan

To meet your immediate financial requirements, you can quickly obtain a loan. Two hours after applying you can get a loan of up to $750. For a loan, the term can range from one day up to sixty-two months. Using its website, app or shop location, it is available in over 120+ retail locations across Canada and the United States. Also available online in Alberta, BC, Manitoba, New Brunswick, Nova Scotia, Ontario, and Saskatchewan.

- Advertisement -

6. My Canada Payday

You may acquire payday loans of up to $1500 in as little as 15 minutes with Online Payday Loans Canada! With My Canada Payday, bad credit isn’t an issue. No credit check is required for the majority of short-term loans because they are secured by an online bank account. TrustPilot users have given My Canada Payday an average rating of 4.6 out of 5 stars.

Applying for a My Canada payday loan online is simple and convenient. Within 15 minutes, you’ll get the money by Interac e-Transfer.

7. Loan Express payday loan

Loan Express payday loans allow you to acquire up to $1500 in as little as five minutes, which can be used to meet unexpected costs that can’t wait until your next paycheck. The maximum borrowing term is 62 days.

8. Pay2day

With a rate of $15 for $100 borrowed, PAY2DAY is in line with the national average. If you’re making at least $1,000 a month, you’ll be able to borrow as much as $1,500 from this lender.

Payday lender PAY2DAY has more than 30 locations across Canada, making it one of the most easily available organizations on our list of payday lenders.